Unlocking Housing Wealth: Professor Isaac Megbolugbe’s Legacy in Reverse Mortgages

Isaac Megbolugbe

April 9, 2026

Introduction

The reverse mortgage market has undergone a significant transformation over the years, evolving into a vital component of the US mortgage market landscape. At the forefront of this transformation is Professor Isaac Megbolugbe, a renowned expert in housing finance and real estate. His groundbreaking work, particularly the 1993 publication “Proceedings: Reverse Mortgages: Improving Housing Market Liquidity,” co-edited with Jide L. Iwarere, shed light on the potential of reverse mortgages to unlock housing wealth for elderly homeowners.

Through his influential research, leadership roles, and innovative approaches, Megbolugbe has played a pivotal role in enhancing liquidity in the reverse mortgage market. This article delves into the life and work of Professor Megbolugbe, exploring his contributions to the development of reverse mortgages, his impact on the US housing market, and his enduring legacy in the field of housing finance.

Pioneering Housing Finance Liquidity

Professor Isaac Megbolugbe played a pivotal role in transforming the reverse mortgage market, significantly enhancing its liquidity and cementing its position as a key feature of the US mortgage market landscape. His influential work was partly documented particularly in the 1993 publication “Proceedings: Reverse Mortgages: Improving Housing Market Liquidity,” co-edited with Jide L. Iwarere, shed light on the potential of reverse mortgages to unlock housing wealth for elderly homeowners.

This publication, stemming from a March 2, 1993, event, explored the role of reverse mortgages in increasing liquidity within the housing market, providing a vital resource for financial literature. The work addressed how elderly homeowners can convert home equity into income, a topic frequently analyzed in financial studies.

Megbolugbe’s contributions didn’t stop there. As Vice President at Fannie Mae from 1990 to 2002, he facilitated the scaling and mainstreaming of reverse mortgage markets, pioneering the use of geographic information technology in the real estate and mortgage industry. This groundbreaking approach has since become standard practice across the sector.

His work has been widely recognized, and he was awarded the Albert Nelson Marquis Lifetime Achievement Award for his leadership in consulting and real estate. Megbolugbe’s legacy continues to shape the industry, with his research and expertise remaining highly relevant.

The Power of Reverse Mortgages: Unlocking Liquidity in the US Mortgage Market

Reverse mortgages have emerged as a vital financial product, playing a significant role in boosting liquidity in the US mortgage market. Much like precision engineering in agricultural practices, which enables optimal irrigation and nutrient delivery to fields, reverse mortgages have transformed the way homeowners tap into their home equity.

What are Reverse Mortgages?

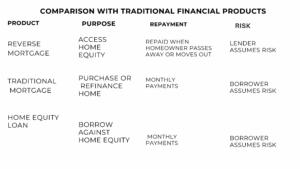

A reverse mortgage is a type of loan that allows homeowners, typically seniors, to borrow money using the equity in their home as collateral. Unlike traditional mortgages, reverse mortgages do not require monthly payments. Instead, the loan is repaid when the homeowner passes away, sells the property, or moves out.

Benefits of Reverse Mortgages

1. Increased Liquidity: Reverse mortgages inject much-needed liquidity into the mortgage market, enabling homeowners to access cash without having to sell their properties.

2. Supplemental Income: Reverse mortgages provide seniors with a steady stream of income, helping them cover living expenses, healthcare costs, or other financial obligations.

3. Flexibility: Reverse mortgages offer flexible repayment terms, allowing homeowners to choose how they receive funds, such as a lump sum, monthly payments, or a line of credit.

Precision Engineering in Agriculture and Reverse Mortgages

Just as precision engineering in agriculture optimizes irrigation and nutrient delivery, reverse mortgages have optimized the way homeowners access their home equity. Both involve:

1. Efficient Resource Allocation: Precision agriculture ensures optimal water and nutrient use, while reverse mortgages allocate home equity efficiently.

2. Risk Management: Both involve managing risk, whether it’s crop failure or market fluctuations, to ensure desired outcomes.

3. Increased Productivity: Precision agriculture boosts crop yields, while reverse mortgages unlock liquidity, stimulating economic activity.

Conclusion

Reverse mortgages have become a crucial component of the US mortgage market, providing homeowners with a valuable tool to access their home equity. By understanding the benefits and mechanics of reverse mortgages, homeowners can make informed decisions about their financial future.

The Enduring Impact of Reverse Mortgages on the Liquidity of the US Housing Market

Reverse mortgages, particularly Home Equity Conversion Mortgages (HECMs), act as a vital liquidity mechanism for aging homeowners, unlocking trapped housing wealth without forcing immediate sales. By providing cash flow, these loans—projected to grow to $2.7 billion by 2030—support senior financial independence but can accelerate equity depletion and create long-term housing market turnover, especially when borrowers face default.

Impact on Housing Market Liquidity

Equity Monetization: Reverse mortgages allow seniors to convert home equity into tax-free cash (often used for healthcare or debt), increasing liquidity for households without requiring them to downsize or move.

Reduced Immediate Turnover: By enabling seniors to stay in their homes, reverse mortgages temporarily decrease the supply of existing homes for sale, as holders often stay longer than they would without the extra liquidity.

Forced Sales and Foreclosures: If borrowers fail to pay taxes/insurance or occupy the home (e.g., move to assisted living), the loan becomes due. Defaults increased from 2% in 2014 to 18% in 2018, which can lead to involuntary foreclosure sales, thereby accelerating the release of that specific home back to the market.

Long-Term Equity Depletion: High interest accrual can lead to “negative equity,” where the loan balance exceeds the home value, shifting the risk to the FHA. This reduces the eventual inheritance and can force accelerated sales of the property, adding to market inventory at that later date.

Market Trends and Growth (2025-2026)

The reverse mortgage market is experiencing a revival, with a projected 7.6% CAGR, driven by high home equity (up 54.9% from 2020-2025) and aging demographics.

Proprietary Growth: Private-label (non-HECM) reverse mortgages are gaining market share (45% of new loans in 2025) because they offer higher loan limits, providing liquidity to high-value homeowners.

Regional Impact: Seniors often take out reverse mortgages when local markets peak, providing them with maximum cash but potentially reducing the available equity for future buyers.

While reverse mortgages offer a crucial, if underutilized, tool for senior income, they essentially “borrow from the future,” temporarily lowering market inventory while creating a long-term, high-risk mechanism for accelerating eventual home sales.

Professor Megbolugbe’s Broader Contributions: The Expansion and Efficiency Mortgage Markets

Professor Isaac Megbolugbe is a seminal figure in the modernization of the U.S. and global housing finance systems. His work has bridged the gap between academic economic theory and the practical efficiency of mortgage markets, particularly through his leadership at Fannie Mae and his research on liquidity-enhancing financial instruments.

Pioneering Reverse Mortgage Liquidity

Megbolugbe’s contributions to the Reverse Mortgage (RM) sector transformed it from a niche product into a sophisticated tool for managing senior housing wealth.

Contracting and Crossover Risk: In his landmark 1994 study, Reverse Mortgages: Contracting and Crossover Risk, he developed foundational pricing models to quantify the “crossover” point—the moment when a loan balance exceeds the home’s value.

Secondary Market Integration: He was a vocal proponent of using securitization and life insurance contracts as secondary market channels, which provided the necessary capital for lenders to offer these non-recourse loans at scale.

Consumption Smoothing: His research demonstrated that RMs allow “house-rich, cash-poor” seniors to achieve consumption smoothing in retirement, effectively unlocking billions in previously illiquid home equity to support living expenses and healthcare.

Advancing Market Efficiency and Scorecards

As a key researcher and executive, Megbolugbe spearheaded the technological shift toward data-driven lending.

Mortgage Scorecards: He pioneered the design and development of mortgage scorecards, which automated the underwriting process. By standardizing risk assessment, these tools reduced human bias and dramatically increased the speed and efficiency of loan approvals.

Predictive Modeling: His work on housing demand and economic modeling at Fannie Mae helped the industry better forecast market cycles, leading to more stable capital allocation across different economic climates.

Global Market Expansion: He applied these U.S.-developed efficiencies to international contexts, advising on the development of mortgage finance markets in emerging economies, such as Nigeria, to overcome local liquidity constraints.

Academic and Institutional Leadership

Beyond his technical innovations, Megbolugbe has shaped the field through high-level institutional roles:

Johns Hopkins University: As a Professor of Practice, he mentored the next generation of real estate leaders, focusing on the intersection of urban land use and finance.

Fannie Mae & NAHB: His leadership at Fannie Mae and the National Association of Home Builders (NAHB) placed him at the center of policy debates, where he advocated for market-based solutions to affordable housing.

Professor Megbolugbe’s legacy lies in his ability to quantify risk in ways that encouraged private and public investment, ultimately making the secondary mortgage market more resilient and accessible.

Urban Development Finance

Professor Isaac Megbolugbe’s contributions to urban redevelopment finance center on the integration of sophisticated risk modeling, spatial data, and institutional capital to revitalize distressed urban areas. His work has transitioned the field from speculative development to a more structured, data-driven discipline that balances private-sector efficiency with public-sector housing goals.

Innovative Financial Frameworks for Urban Markets

Megbolugbe’s approach to urban finance emphasizes “market-making” in areas traditionally viewed as high-risk by commercial lenders.

Risk Mitigation in Distressed Zones: He leveraged his expertise in mortgage scoring to create frameworks that accurately price risk in urban redevelopment projects. By standardizing how risk is measured, he encouraged institutional investors to provide the liquidity necessary for large-scale urban revitalization.

Secondary Market Access: During his tenure as Vice President at Fannie Mae, he was instrumental in developing financial products that allowed urban redevelopment loans to be packaged and sold in secondary markets. This process lowered the cost of capital for developers working on affordable and mixed-income housing in core city neighborhoods.

Consumption and Demand Modeling: His research on housing demand helped urban planners and developers understand the specific economic drivers of city-center growth, moving beyond broad suburban models to address the unique demographics of urban renters and buyers.

Spatial Intelligence and Urban Investment

A hallmark of Megbolugbe’s work is the pioneering use of Geographic Information Systems (GIS) to drive investment decisions.

Targeted Revitalization: He championed GIS as a standard tool for identifying “undelivered” urban markets where infrastructure existed but capital was lacking. This allowed for hyper-local investment strategies that could target specific blocks for redevelopment.

Predicting Neighborhood Change: Building on the work of scholars like William G. Grigsby, Megbolugbe developed models to forecast neighborhood change and turnover. This predictive capability is essential for urban redevelopment finance, as it helps investors identify areas poised for growth before land values peak.

Bridging Policy and Practice

Megbolugbe has consistently applied these financial theories to real-world urban challenges through his roles at Johns Hopkins University and Linneman Associates.

Strategic Advisory: Through GIVA International, he has provided strategic guidance to governments on urban land use and finance, particularly focusing on how to use public funds to leverage private investment.

Mentorship in Urban Finance: As a Professor of Practice, he has shaped the curriculum for future real estate leaders, emphasizing that modern urban redevelopment must be both financially viable and socially responsible.

Professor Megbolugbe’s work fundamentally changed how urban space is viewed by the financial sector—shifting it from a “risky” outlier to a quantifiable and essential component of the national housing finance system.

Urban Market GIS Pilots

While Professor Megbolugbe’s GIS-based frameworks were designed for broad national application, several specific urban markets and regions were central to the early development, testing, and implementation of these models during his tenure at Fannie Mae and his academic research.

The following areas represent key markets where his work on spatial intelligence and mortgage scoring was notably applied:

Primary Pilot and Development Markets

Washington, D.C. Metropolitan Area: As his base of operations at Fannie Mae and later Johns Hopkins University, D.C. served as a primary “living lab.” He used GIS to map local underserved neighborhoods, helping to transition the city’s housing finance from stagnant traditional lending to dynamic, data-driven reinvestment strategies.

Philadelphia, PA: Megbolugbe conducted significant early research in Philadelphia, particularly focusing on neighborhood change and turnover models. This work was critical in identifying how to price mortgage risk in aging urban cores where traditional appraisal methods often failed to capture emerging value.

Baltimore, MD: Through the Johns Hopkins Carey Business School, he utilized GIS-based models to analyze urban redevelopment finance in Baltimore. These models helped target specific blocks for the revitalization of distressed properties, bridging the gap between municipal planning and private capital.

Strategic Regional Implementations

Underserved “Goal” Markets: Under Megbolugbe’s leadership, Fannie Mae utilized GIS to meet federally mandated “underserved areas” goals. This involved intense data mapping in major urban centers like Chicago, Los Angeles, and New York City to identify census tracts where mortgage credit was artificially constrained.

Emerging International Markets (Nigeria): Megbolugbe applied his GIS-based mortgage models to Nigeria’s burgeoning housing market. He worked with local institutions to pilot scoring systems in cities like Lagos and Abuja, aiming to create the first structured secondary mortgage market in the region by quantifying risks that were previously considered unmanageable.

The “GIS Primer” Legacy

His seminal 1998 work, A Primer on Geographic Information Systems in Mortgage Finance, established the technical blueprint for using these markets as prototypes. By demonstrating how to track defaults and mark portfolios to market using spatial data, he provided the toolkit that eventually allowed lenders to scale these “pilots” into a standard national practice.

Concluding Remarks

In conclusion, Professor Isaac Megbolugbe’s contributions to the reverse mortgage market have been nothing short of transformative. His pioneering work, particularly the 1993 publication “Proceedings: Reverse Mortgages: Improving Housing Market Liquidity,” has had a lasting impact on the industry, enhancing liquidity and cementing reverse mortgages as a vital component of the US mortgage market landscape.

Through his research, leadership roles, and innovative approaches, Megbolugbe has demonstrated a deep understanding of the complex relationships between housing finance, economic development, and social welfare. His work has not only advanced the field of housing finance but also improved the lives of countless individuals, particularly elderly homeowners, by providing them with greater financial flexibility and security.

As the reverse mortgage market continues to evolve, Megbolugbe’s legacy serves as a powerful reminder of the importance of innovation, research, and collaboration in shaping the future of housing finance. His contributions will undoubtedly continue to inspire and inform industry professionals, policymakers, and researchers for years to come.

In the end, Professor Megbolugbe’s work is a testament to the profound impact that dedicated individuals can have on their chosen field. His commitment to advancing the field of housing finance has left an indelible mark, and his legacy will continue to shape the industry for generations to come.

Isaac Megbolugbe, Director of GIVA Ministries International. He is a recipient of Albert Nelson Marquis Lifetime Achievement Award in business and academia in the United States of America. He is retired professor at Johns Hopkins University and a Fellow of the Royal Institution of Chartered Surveyors. He is resident in the United States of America.